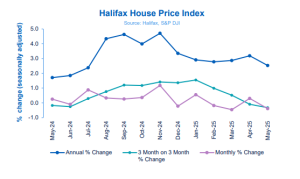

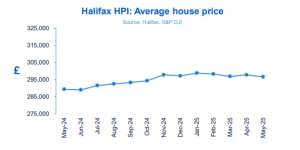

The Halifax House Price Index, the UK’s longest running monthly house price series, released its index for May 2025 last week.

From data covering the whole country going back to January 1983, a “standardised” house price is calculated and property price movements on a like-for-like basis (including seasonal adjustments) are analysed over time. The annual change figure is calculated by comparing the current month seasonally adjusted figure with the same month a year earlier.

Amanda Bryden, head of mortgages at Halifax, said: “These small monthly movements point to a housing market that has remained largely stable, with average prices down by just -0.2% since the start of the year. The market appears to have absorbed the temporary surge in activity over spring, which was driven by the changes to stamp duty.

“Affordability remains a challenge, with house prices still high relative to incomes. However, lower mortgage rates and steady wage growth have helped support buyer confidence.

“The outlook will depend on the pace of cuts to interest rates, as well as the strength of future income growth and broader inflation trends. Despite ongoing pressure on household finances and a still uncertain economic backdrop, the housing market has shown resilience – a story we expect to continue in the months ahead.”

Responding to the data, Jonathan Handford, managing director at national estate agent group Fine & Country commented: “House prices saw a modest decline in May, reflecting the market’s ongoing adjustment after a transitional start to the year.

“This slight month-on-month dip follows the stamp duty changes introduced in April and comes just ahead of the typically quieter summer period, when many families pause moving plans to focus on holidays and school breaks.

“Although economic pressures continue to impact personal finances, with inflation at 3.5% and household budgets feeling the squeeze, the Bank of England’s May rate cut to 4.25% has offered some welcome relief. While mortgage rates remain relatively high, any further easing in borrowing costs could help reignite market activity.

“Mortgage approvals fell in April as demand naturally cooled after the stamp duty tax break ended, and tighter lending criteria and deposit requirements still pose challenges for many buyers, particularly first-time purchasers. However, steady wage growth is providing some support, even if affordability remains a hurdle.

“Overall, May’s price movement highlights ongoing headwinds but also points toward potential for recovery. The recent flurry of transactions would have been welcomed by sellers and a quieter period was always to be expected.

“A sustained upturn will rely on broader economic improvements and targeted efforts to enhance affordability, fostering a healthier and more balanced housing market in the months ahead.”

Babek Ismayil, founder and CEO of homebuying platform OneDome, was less optimistic about index’s findings, commenting: “Despite the turbulence, the market is largely stable – a fact that will give some reassurance to home-owners, but it’s not plain sailing in the short term.

Babek Ismayil, founder and CEO of homebuying platform OneDome, was less optimistic about index’s findings, commenting: “Despite the turbulence, the market is largely stable – a fact that will give some reassurance to home-owners, but it’s not plain sailing in the short term.

“Optimism about falling interest rates seems to be premature, as Trump’s hokey-cokey trade wars fuel turbulence in the economy. Expected reductions in interest rates may not come as soon as predicted, dashing the hopes of home-owners on variable mortgages and first-time buyers. Affordability is still stretched for first-time buyers, particularly in the South, but there’s more homes on the market as mortgage availability improves. If we’re serious about sustained growth, we need to invest in the infrastructure of buying a home. A streamlined, digital-first process that brings estate agents, brokers and conveyancers into one platform is the only way to reduce friction and restore long-term confidence in the market.”