Glenigan has released its widely anticipated UK Construction Industry Forecast 2022-2024.

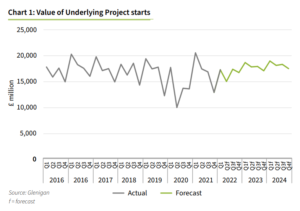

The key takeaway from this Forecast indicates the construction industry will face challenging economic conditions. However, whilst growth will be stifled in 2022 (-2%), 2023 is predicted to see a modest 8% increase and a smaller 2% lift in 2024, representing an average rise of 2.6% over the Forecast period.

This report is predominantly focused on underlying starts (< £100m in value), unless otherwise stated, and contains a comprehensive overview of the current state of the construction industry. Crucially, it provides overall sector and vertical-specific insight into performance over the next few years.

Significant disruption stifles short-term growth

The next few years will be challenging for the construction industry as a whole. The war in Ukraine is creating considerable economic uncertainty which is having a direct, current effect on output, derailing post-COVID recovery. As a result, overall project starts are forecast to slip back 2%.

Aside from this ongoing conflict, current inflation spikes, higher taxes and rising mortgage costs are expected to constrain activity in consumer-related areas, such as private housing, retail and hotel & leisure.

In contrast, a firm development pipeline is predicted to lift industrial and office starts in 2022, as well as Government-funded areas such as education, health and community & amenity.

More positively, the value of project starts is expected to rise in 2023, as the UK economy stabilises and short-term supply chain pressure ease. However, the lingering impact of higher construction, material and energy costs means this growth will be significantly lower than predicted in previous forecasts.

Housing Starts Depressed

Although a buoyant housing marked helped to lift new housebuilding activity in 2021, with starts rising 26%, this recent surge is fading.

Predicted to drop 5% in 2022, following the removal of temporary Stamp Duty relief and dwindling homebuyer confidence, higher taxes and mortgage costs, housebuilders are expected to moderate project starts and focus on building out developments already on-site.

However, this slowdown appears temporary, with a renewed build-for-sale starts recovery anticipated in the second half of the Forecast period, rising 14% in 2023 and 1% in 2024, as household financial positions and UK economic prospects improve. Furthermore, a strong development pipeline has also be registered for Build-to-Rent starts, following a productive 12 months in 2021.

Bright spots for non-residential work

Industrial starts, particularly warehouse and logistics, are set to remain a growth area, building on the ever-increasing appetite for online retail, which accelerated during the pandemic. With e-commerce expected to be a significant growth market in the coming years, 2022 will see start value increase by 11%.

However, the online shopping boost has hit physical retail hard, with high street and outlet footfall remaining far lower than pre-pandemic levels. Unsurprisingly, lower consumer spending power, an overhang of empty retail premises and a greater share of the market moving online, means growth will be tempered over the Forecast period. Here, increased investment by the deep discount supermarkets, Aldi and Lidl, will be the primary drivers of the predicted 6% average uplift between 2022 and 2024.

The leisure and hospitality sector, hit hard by the pandemic, is also only set to expect modest recovery over the Forecast period due to reduced consumer discretionary spending during a tighter economic climate.

Moving from play to work, office starts bounced back sharply last year (+27%) and are predicted to benefit over the forecast period (av. +11%). This potential growth can be attributed to a rise in refurbishment projects as tenants and landlords adapt premises to accommodate changing working practices. However, new build office projects will likely be slower to recover as tenants and developers assess the effects of the shift towards remote and hybrid working on the long-term demand for office accommodation.

Public Sector Pick-Up

Public sector investment is set to be an important driver for construction activity over the Forecast period. However, the latest Spending Review revealed only modest growth in capital funding for a handful of central Government departments over the next three years.

Whilst the value of social housing starts is set to dip almost 10% this year, following a 15% surge in 2021, the vertical is predicted to rally for the remainder of the Forecast period, helped by a strong pipeline of already approved projects commencing on site.

Education construction is a vertical predicted to grow significantly over the next few years (av. +8%), partly driven by the Government’s commitment to building 500 new schools over the next decade. This is supported by a modest rise in universities capital spending during the second half of the Forecast period

The outlook for the health sector is also brightening. Starts remained high in 2021 post-Pandemic and the increase in capital funding and a growing development pipeline means the value of starts are expected to remain steady over the Forecast period, will slight declines this year (-5%) and next (-6%) .

Focusing on civils and infrastructure, a significant funding increase in areas such as roads, especially to address the maintenance backlog on the nation’s local roads, is helping to lift the value of project starts.

Investment in rail projects and utilities development, as well as ongoing work on major infrastructural projects such as Thames Tideway, HS2 and Hinkley Point are also set to support vertical activity over the Forecast period.

Allan Wilen, Glenigan’s economic director, said: “Circumstances have changed significantly since the November 2021 Forecast and, whilst the short-term picture appears challenging, we should adopt a sanguine approach for the next few years. Markets sent into turmoil by the Russia-Ukraine War are starting to stabilise as new supply chain solutions are developed and established.

“Of course, in the near future construction and building product costs will remain high. However, this situation will no doubt encourage a burst of imagination and innovation which will see the sector weather the current storm and progress to, if not sunny uplands, then at least towards a trajectory of upward growth.”